Weekly Chart Review

New all-time highs in sight or a continued rotation into the defensives from a couple weeks ago?

Happy Monday!

On a year-to-date (YTD) basis, the market continues to be driven by the “Big 3” (Communication Services, Technology, and Consumer Discretionary).

Further, note the bifurcation of returns between what I’m calling the “leaders” and “laggers” which I have separated with a yellow vertical dashed line in the chart below.

On a YTD basis, the “leaders” have achieved an average return of +29.2% (green horizontal dashed line) vs. an average return for the “laggards” of +1.4% (red horizontal dashed line).

Note: S&P 500 values have been excluded from all “leaders/laggards” average calculations.

Last week, I noted that the “laggards” had fairly dramatically outperformed the “leaders” for the week ending 07/21/23. Fast forward to the week ending 07/28/23, and we saw a bit of a reversal.

With that said, if we look at the last two weeks, we find that the “laggards” are still outperforming the “leaders” which suggests that the “leaders” outperformance from last week was not enough to overcome the “laggards” outperformance the previous week.

This is a development that we will need to monitor in the weeks to come because I firmly believe that when the market begins to turn, it will include a rotation out of the “leaders” and into some or all of the “laggards”.

Further, pay close attention to the Energy sector as it has dramatically outperformed all other sectors over the last two weeks. If energy prices continue to rise, this will feed through to inflation figures which means the FOMC could be poised to raise rates further this year.

As of right now, Fed Funds futures (as shown in the table above) have priced in no additional rate hikes this year. This could change if energy prices continue to rise and GDP continues to surprise to the upside as it did with last week’s 2.4% print.

Absolute Value & Relative Value Charts

Here are the weekly updates for my absolute value and relative value charts.

Absolute Value

As has been the case for many months, the vast majority of the market remains camped out in the upper-right “Expensive & Overbought” quadrant.

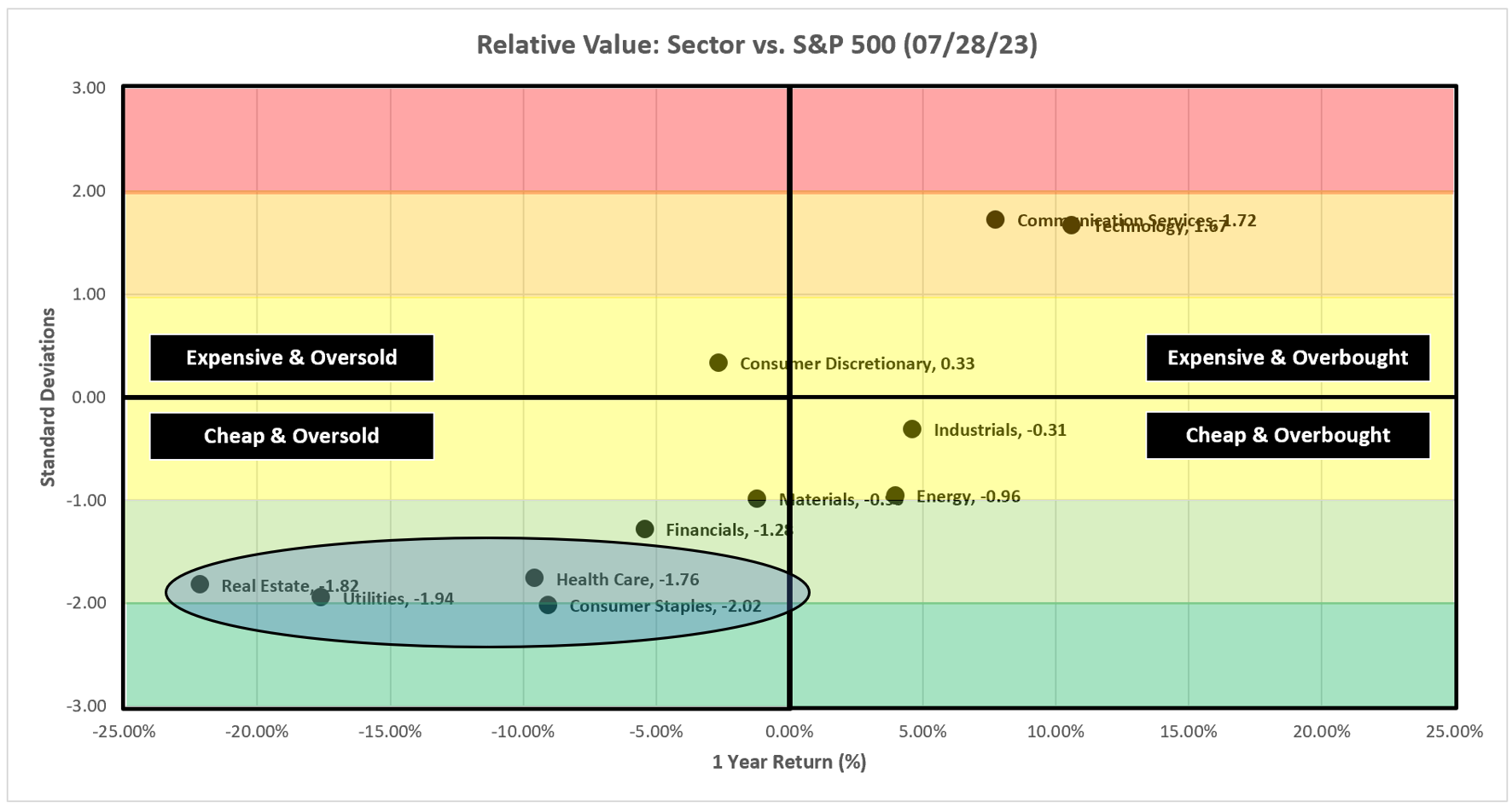

Relative Value

Most of our “laggards” remain in the bottom-left “Cheap & Oversold” quadrant. With that said, they have “moved up” over the last couple of weeks as they have had better performance on a relative basis.

Let’s close out by taking a look at the individual charts. I’ll start with the S&P 500 and then run through each of the sector charts.

S&P 500 Index

Positive:

The uptrend remains intact and the target remains 4,927.

Negative:

Watch the RSI, it is very close to the level where we’ve seen a pullback begin. If we do see a pull-back, bulls will need to see the moving averages provide support for the target to remain intact.

Technology

Positive:

The uptrend remains intact and the target remains 190.75.

XLK appears to be shaking off the potential “Shooting Star” candle that I alluded to last week.

Negative:

Watch the RSI, it is very close to the level where we’ve seen a pullback begin. If we do see a pull-back, bulls will need to see the moving averages provide support for the target to remain intact.

Communication Services

Positive:

The uptrend remains intact and the target remains 74.80.

Negative:

Watch the RSI, it is very close to the level where we’ve seen a pullback begin. If we do see a pull-back, bulls will need to see the moving averages provide support for the target to remain intact.

Consumer Discretionary

Positive:

The uptrend remains intact and the target remains 196.55.

Negative:

While the uptrend technically remains intact, I think it is important to take note of the “rounding top” we have begun to see over the last few weeks. Couple this with the “trouble” XLY has had getting past the high from one year ago and these could be signs of a potential move lower. Watch for the moving averages to provide support.

Industrials

Positive:

The uptrend remains intact and the target remains 125.13.

Negative:

There’s not a lot to dislike about this chart. Moving averages are positively sloped, RSI has room to run, and the target suggests XLI may still have some gas left in the tank.

Materials

Positive:

The uptrend remains intact and the target remains 102.85.

Negative:

Similar to the Industrials chart, there’s not a lot to dislike about this chart.

Energy

Positive:

A close above the “right shoulder” (87.66) negates the Head & Shoulders pattern and creates a target of 111.94 which would suggest that the Energy sector may have some fairly substantial room to run.

Negative:

The above scenario is moot without a close above and a continuation beyond the 87.66 threshold.

Financials

Positive:

RSI remains in an uptrend and above the midline.

Negative:

Did XLF finally create the “right shoulder” of the Head & Shoulders pattern? I’m not sure so watch to see what happens when it comes in contact with the moving averages. If they provide support, that is clearly a good thing. If not, XLF is likely going to the neckline (30.40).

Real Estate

Positive:

If I’m honest, there’s not much to like about this chart. The downtrend continues, XLRE can’t break free from the triangle pattern, RSI is rolling over, etc.

Negative:

See above.

Consumer Staples

Positive:

This chart continues to make me think of the book “The Little Engine That Could”. XLP has been in a trading range for the vast majority of the last year and a half. If it can break through the neckline (77.93), it has a chance to run to 89.36.

Negative:

The above scenario is moot if the neckline cannot be achieved and thus far, the range from 75.00 - 78.00 has been tough to break through.

Utilities

Positive:

Prior to the last week, we’d had several weeks that suggested XLU could be on its way to making a breakout. Last week’s reversal did not help its cause.

Negative:

RSI is breaking lower, moving averages remain downward sloped, and XLU made its way back into the triangle pattern.

Health Care

Positive:

Despite the setback last week, the target remains 149.34 but XLV really needs to clear the 23.6% Fibonacci level of 136.69.

Negative:

RSI moved lower last week and the 23.6% Fibonacci level has now proven to be resistance on multiple occasions.

Summary

I think the third quarter of this year could end up being an interesting inflection point for the market.

As it stands right now, we’ve got the S&P 500 and several sectors poised to make new all-time highs. Alternatively, if we continue to see the “laggards” pick up steam relative to the “leaders”, I think this could be indicative of a topping market.

Lastly, watching the Energy sector and the GDP numbers from last week, I’m not convinced that inflation has been tamed to the degree that the FOMC has the ability to fly the “Mission Accomplished” banner.

If that is the case, more rate hikes are in store and the market is not pricing that in right now. All else being equal, equities tend to frown upon the idea of additional (and unexpected) rate hikes.

Never a dull moment.

Until next week…

Thanks. So helpful!

Great summation of charts & commentary; thank you.