Weekly Chart Review

Tariffs = Buying Opportunity?...AND...Sector Specific Price Targets

Before we jump into this week’s newsletter, I want to tell you about a special offer we are running for this week only!

If you become a paid subscriber between now and February 17th, you will receive 70% off the annual rate and you will lock in this rate forever!

Our annual membership is typically $396/year. For the next week, we are offering a 70% discount which brings the price to $119 or the equivalent of $9.90/month.

Don’t miss this opportunity to get the Weekly Chart Review!

We have seemingly entered an environment at the National level whereby the primary negotiating tool has become the threat of tariffs.

Interestingly, Columbia, Mexico, and Canada folded within hours of said tariffs potentially taking effect. China has been a bit more resilient and countered with its own tariffs.

It looks like the tariff threat won’t stop there as the following headlines came out on Friday (quoting from Reuters below):

“President Donald Trump said on Friday he plans to announce reciprocal tariffs on many countries by Monday or Tuesday of next week, a major escalation of his offensive to tear up and reshape global trade relationships in the U.S.' favor.

Trump did not identify which countries would be hit but suggested it would be a broad effort that could also help solve U.S. budget problems.

"I'll be announcing that, next week, reciprocal trade, so that we're treated evenly with other countries," Trump said. "We don't want any more, any less."

We can debate the effectiveness of tariffs over the long term, but they have certainly been used effectively over the short run to obtain the actions and/or concessions that President Trump desires.

With that said, tariff threats cause distortions in global markets.

The knee-jerk reaction is typically as follows:

Threat of tariffs —> commodity prices rise —> US Treasury yields rise —> equities decline.

Then, when the tariff threat subsides and/or concessions are made, the opposite occurs:

Concessions made —> commodity prices fall —> US Treasury yields decline —> equities rise.

I am making generalizations here but you get the picture.

It would seem that no country (with the possible exception of China) has the stomach for US-imposed tariffs on their country.

This leads me to believe that until proven otherwise, we should fade the initial move and operate under the assumption that concessions will be made.

Valuation Metrics

Let’s take a spin through our valuation metrics and then we’ll jump into sector-specific price targets.

We should start by recognizing that US equities generally are “Expensive & Overbought”.

This has been the case for some time and it is important to remember that markets can remain “Expensive & Overbought” for longer than you think.

With that said, there is always a point at which sanity returns (see the “Average Investors Allocation to Equities” chart at the bottom of this post).

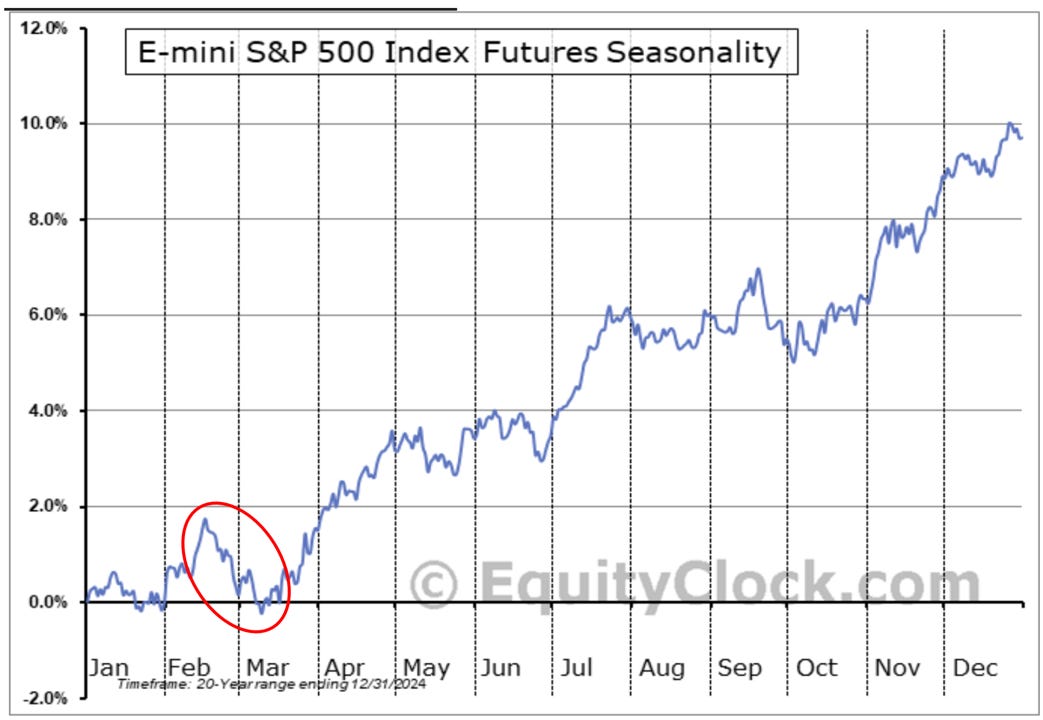

Seasonality

Seasonality also plays a role.

Note how the second half of February into the first half of March has historically played out for the S&P 500.

Is this the case every year, no, but it happens often enough that the 20-year average is what we see in the chart below.

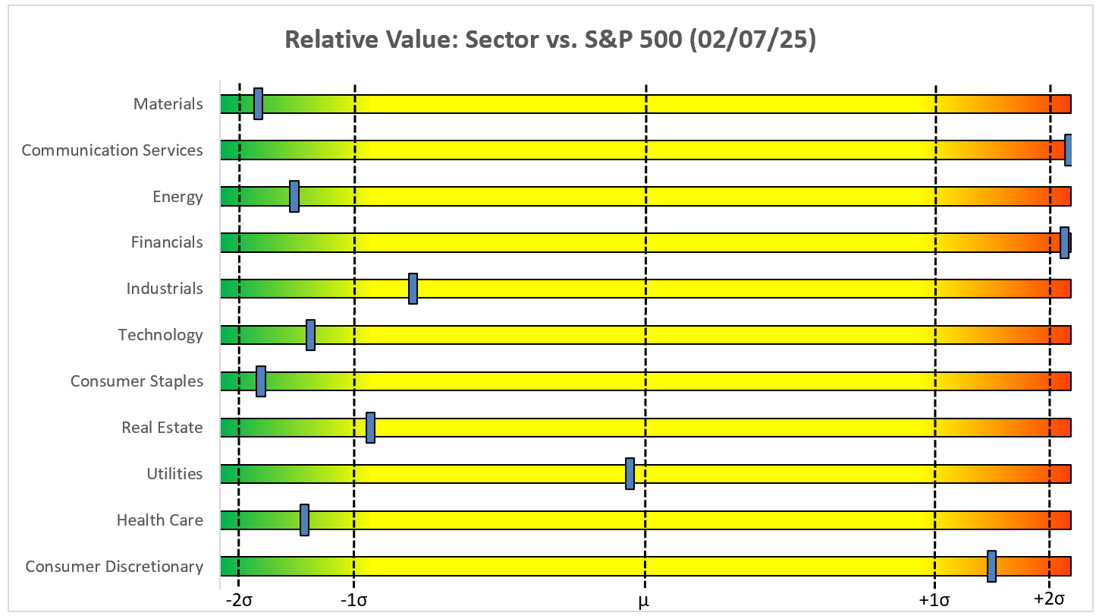

Sectors

Now, let’s drill down to the major US sectors and compare their performance vs. the S&P 500.

This chart tells a bit of a different story. You can see below that Communication Services, Financials, and Consumer Discretionary are the driving forces behind the market’s “Expensive & Overbought” position.

Here’s another view.

Let’s take a look at the charts.

Keep reading with a 7-day free trial

Subscribe to Skillman Grove Research to keep reading this post and get 7 days of free access to the full post archives.