Weekly Chart Review

A crude reality...

Happy Monday…let’s dive right in.

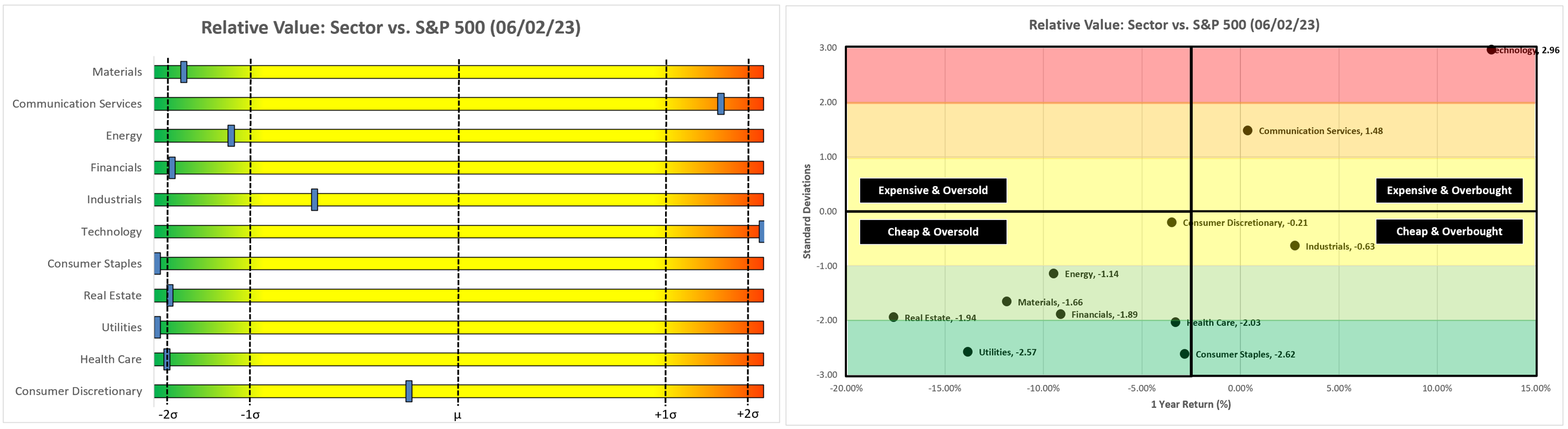

We’ll start, as usual, with our “absolute value” chart. The overarching theme remains the same which is that Technology continues to lead the pack and remains almost 3.0 standard deviations “Expensive & Overbought”.

The Communication Services sector moved from 2.02 to 2.20 standard deviations thus getting more “expensive” and more “overbought”. Maybe even more important to note is that the S&P 500 has now crossed the 2.0 standard deviation mark.

As I have said a number of times before:

“Typically, when any asset gets north of 2.0 standard deviations, this is where you would begin to look for either a corrective pullback or a consolidation move sideways.

It doesn’t mean that a corrective pullback or a consolidating move sideways will happen immediately, but your antenna should be up the longer (insert asset class) remains above 2.0 standard deviations.”

Moving now to our “relative value” chart. Again, same song we have had for a number of weeks which is that Technology continues to be the outlier as it remains extremely “Expensive & Overbought” relative to the S&P 500.

As noted above, the S&P 500 has now crossed the 2.0 standard deviation mark on an absolute basis. If the S&P 500 were to begin to pull back, investors would likely seek the perceived shelter of the defensive sectors such as Utilities, Health Care, and Consumer Staples. Note that each of these sectors are firmly in the “Cheap & Oversold” quadrant thus making them a good candidate for a relative value trade by investors.

Additionally, we got the following headlines over the weekend:

“Saudi Arabia said Sunday it would cut 1 million barrels of oil a day…”

“Saudi Arabia said the output cut was for July and on top of previously announced curbs, which would be extended until the end of 2024. The United Arab Emirates and some other large producers also extended their previously announced cuts.”

“A cut in production was expected to prop up crude prices amid concerns that a slowing global economy would crimp energy demand.”

As the last quote would suggest, this will likely lead to a short-term increase in crude and energy prices in general. Note that the Energy sector is firmly entrenched in the “Cheap & Oversold” quadrant thus making it a good candidate for a relative value trade by investors.

Crude Oil

The last two production cuts were in October ‘22 and April ‘23. Note that in October, crude oil prices rose to 93.64 and in April, crude oil prices rose to 83.53 after the announced production cuts.

From a technical standpoint, we have a symmetrical triangle pattern that has formed which broke out today on the news of the latest round of production cuts. The pattern calls for a target of 87.16 but will likely face resistance as we approach the April high of 83.53. Net/net, crude oil, and energy prices in general, are poised to move higher.

Rates

A move higher in energy prices tends to be at least directionally inflationary. It certainly depends on how long the price increases last and how much said energy price increases begin to curb demand for other consumer goods. We won’t know that answer for several weeks/months but we’re already seeing yields move higher across the Treasury curve.

Here is a chart of the US Treasury 2 Year yields. I think it is reasonable to suggest that an inverse Head & Shoulders pattern has formed and not only that, the market has come back to test the neckline thus giving the pattern more validity.

Should this pattern continue to play out, the target calls for a US Treasury 2 Year yield of ~4.95%. The US Treasury 2 Year tends to correlate well with Fed Funds; therefore suggesting that further rate increases by the FOMC could be in store if the US Treasury 2 Year yields continue to increase.

Technology

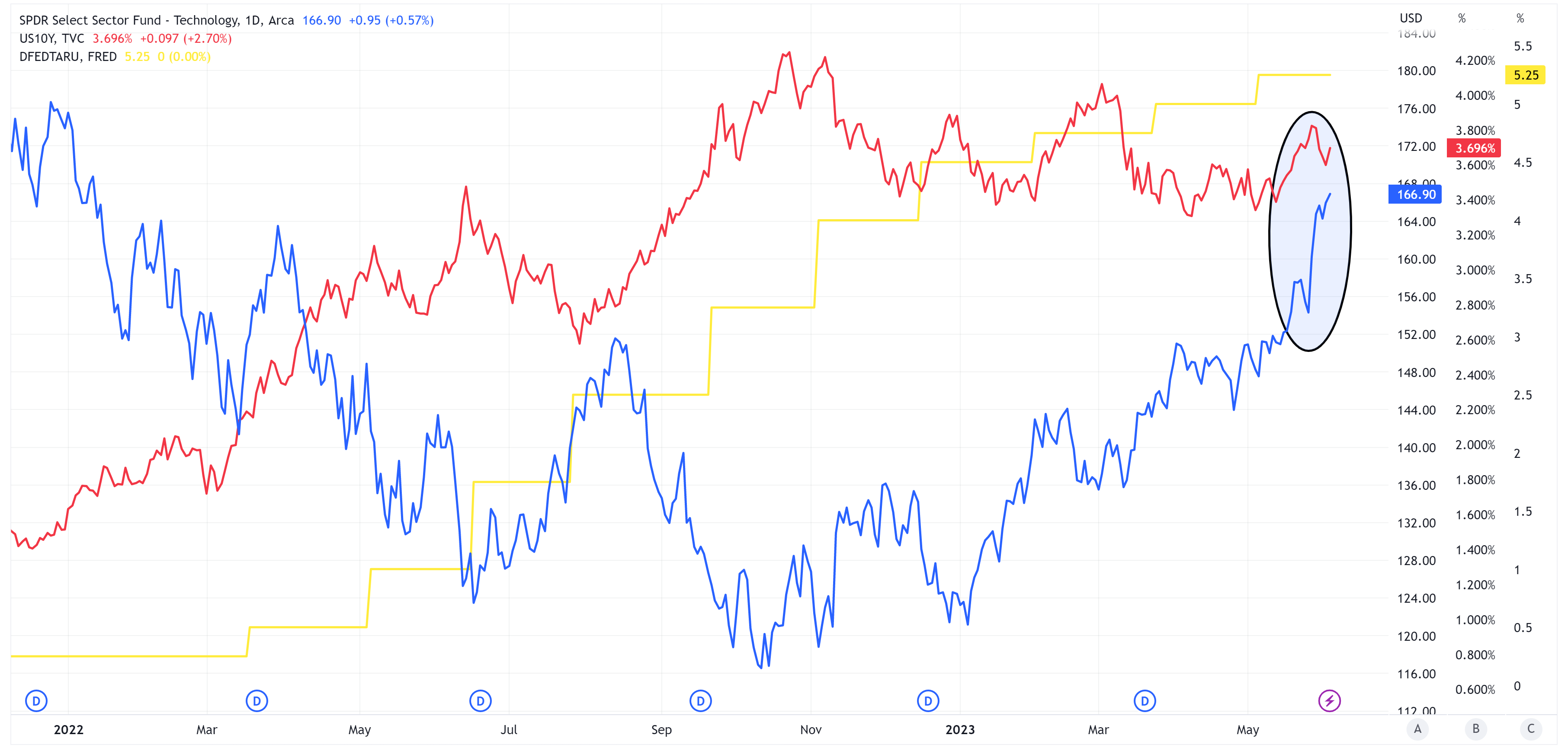

I recently posted the following chart and made the following observation.

“The Technology sector is very sensitive to interest rates. In the following chart, I am showing the Technology sector (blue) vs. the yield of the 10-year US Treasury (red) and I have added the Fed Funds rate (yellow) for reference.

What you find is that the red and blue lines are almost perfectly negatively correlated. Simply meaning that when rates increased, the Technology sector decreased and vice versa.

More recently, we have entered a new paradigm where rates have been increasing (red line) and the Technology sector (blue line) has continued to appreciate. This is counter to what has happened since the beginning of the rate hiking campaign in March of 2022. Will it continue? I don’t know but it’s worth watching.”

Is this “new paradigm” shifting back to what we’ve seen over the last couple of years? If so, that would call for the Technology sector to move lower as rates (yields) press higher.

I have said for weeks that the Technology sector has been driving the market higher on a YTD basis. The WSJ published an article (“Bearish Bets Against S&P 500 Are Surging, Despite Love for Big Tech”) over the weekend that made the following observation:

“The S&P 500 is up 12% this year, but it would be negative without the contribution of seven big tech companies, according to S&P Dow Jones Indices data through the end of May. That potentially leaves the index vulnerable to a steep pullback if even one or two big companies misstep.”

Conclusion

While no one has a crystal ball as to how this will all play out, if we connect the dots, we find that we have an equity market that is reasonably “Expensive & Overbought” and the primary sector driving the equity market is extremely “Expensive & Overbought”. Does that mean that they will begin to pull back this week? No, but we should be watching for that possibility at least in the coming weeks.

Further, we now have a catalyst for higher energy prices which by its nature is inflationary thus suggesting an increase in rates and raising the probability of further rate increases by the FOMC.

Higher rates tend to be problematic for the Technology sector thus suggesting a modest correction in the sector. As goes Technology, so goes the overall market, at least more recently. It’s all circular.

Until next time…