Happy President’s Day!

Last week, the much-anticipated inflation data came in “hotter-than-expected”.

The “hotter-than-expected” inflation data had a direct impact on equities (lower prices), bonds (higher yields), and Fed Funds rate cut projections (higher for longer).

Equities

The following chart is a 30-minute chart of the S&P 500 futures. You can see clearly when the CPI and PPI were released and what the market thought about said reports.

Bonds

Here is the same 30-minute chart but instead for the US Treasury 10-year note.

Rate Cut Projections

A week ago, Fed Funds futures were pricing in a 52.2% chance of a 25 basis point rate cut in May. This has now fallen to only a 35.2% chance of a rate cut and a 61.6% chance of “no cut” in May.

As it stands today, Fed Fund futures are suggesting that the first cut will not happen until June and that there will only be four rate cuts in 2024.

At the beginning of this year, the market was convinced that there would be seven rate cuts in 2024 and that the first one would be in March.

I will go on record as saying that the Fed is not cutting rates until “something breaks”.

Think about it from the Fed’s standpoint, the absolute worst possible outcome is to cut rates too early and reignite, and/or add to the inflationary concerns.

That’s exactly what we saw in the 1970s and it took keeping rates at almost 20% for most of 1980-1981 to finally break the back of inflation (see chart below).

To the Fed’s credit, I think they are enough of a “student of history” that they will err on the side of not cutting, and allowing a recession to take hold before they will “cut just to cut”. The downside of “cutting just to cut” is substantially worse than “allowing” a mild recession to take hold and I think the Fed knows this.

With that said, I don’t believe the Fed is willing to say this publically (i.e., “We’re going to let this go until something breaks…”) so every Fed speech or press conference will be full of commentary that suggests: “We continue to believe that a soft landing is possible…” or “We will continue to be data-dependent…” I’ve come to believe that “data-dependent” is code for “We have no idea what we’re going to do next and we’re just trying to buy some time…”

The conundrum…

This leaves us with a conundrum in that we have an equity market that looks like it wants to continue to run higher yet if I’m correct, we’ve got a Fed that is faced with no really good options other than to wait and see what happens.

I think this puts us in the “plan for the worst, hope for the best” category.

“Planning for the worst” would suggest that we start pre-positioning now for the moment that “something breaks”. Unfortunately, we never know in advance when that will be or what will cause “something to break” but, fortunately, we do know how the Fed will respond. They will cut rates, and likely very aggressively.

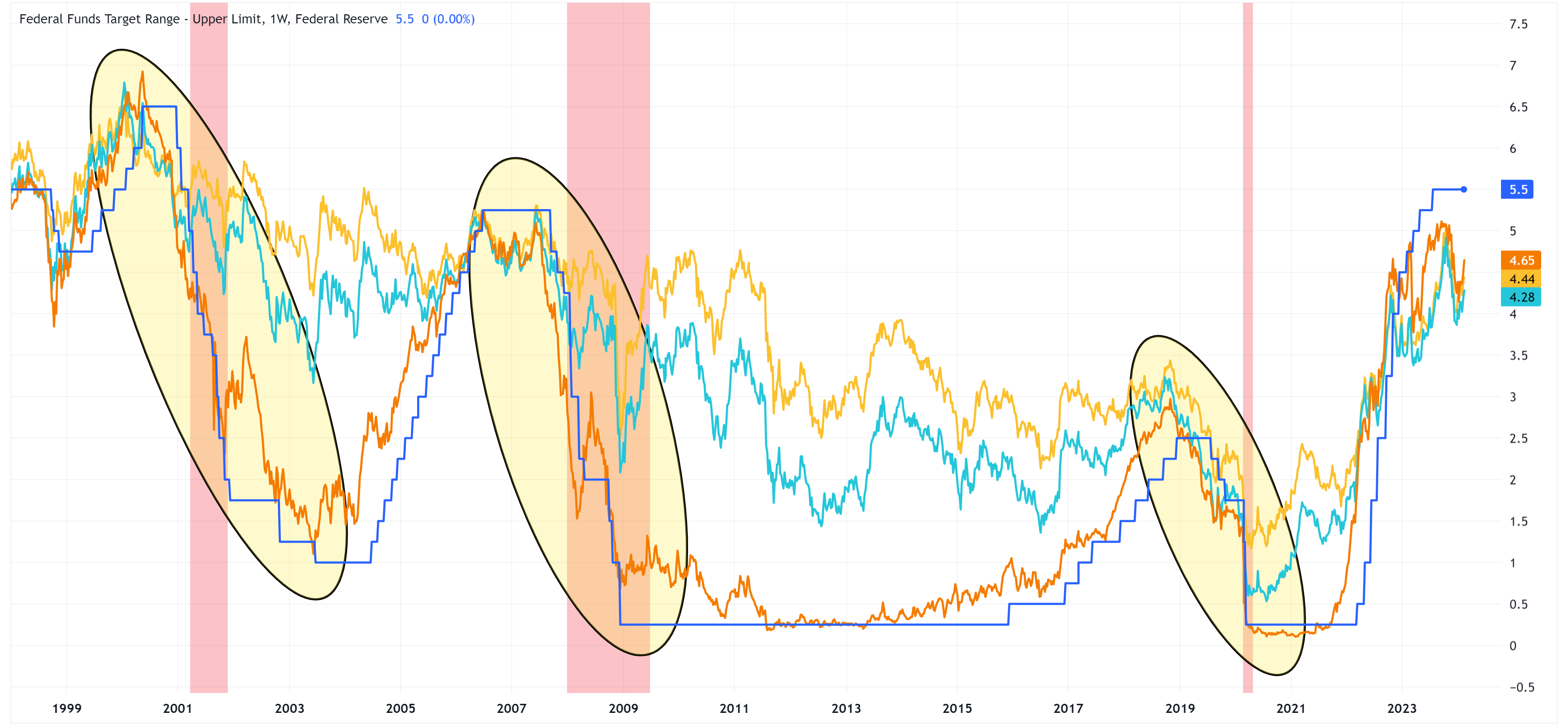

In the chart below, I am showing the Fed Funds target rate (blue line) along with the yields for the UST 2-year, UST 10-year, and UST 30-year.

When “something breaks”, the Fed will cut rates aggressively, and in doing so, the entire US Treasury curve will shift lower in response.

This is when it will be advantageous to own products like ZROZ, TLT, TLH, IEF, and IEI. You can see in the chart below how these investment vehicles performed in the last two aggressive rate-cutting campaigns.

Keep reading with a 7-day free trial

Subscribe to Skillman Grove Research to keep reading this post and get 7 days of free access to the full post archives.