To set the stage for this week, I would like to address two subscriber questions that I received this week:

Can you provide your thoughts on where you think yields will go for the US Treasury 2-year, US Treasury 5-year, and US Treasury 10-year and the implication for markets?

Can you add Uranium to the list of commodities that you track?

The goal is to make this newsletter as interactive as possible and more importantly, as useful as possible for all our subscribers so keep the questions and comments coming!

In addition to these items, we’ll take a look at which asset classes/sectors made the biggest moves last week and where they may be heading this week. We’ll conclude by looking at our “Average Investors Allocation to Equities” model to get a better sense of where the S&P 500 currently stands relative to its “fair value”.

Let’s dive in!

The Fed is in a pickle…

The two most important inflation measures, CPI & PPI, came out last Thursday and Friday, respectively.

You can see in the table below that CPI came in a bit on the “hot” side while PPI came in a bit on the “soft” side.

It seems that the market chose to focus more on the “soft” PPI print instead of the “hot” CPI print. We can see this in how the market reacted relative to its pricing of the next Fed Funds rate change.

When we look at the Fed Funds futures for the next meeting on January 31st, we see that there is currently a 95.3% chance that the Fed will not move rates at that meeting. Further, note that the probability remained virtually unchanged from a week ago.

Fast forward to the March 20th meeting, and we find that Fed Funds futures are not only pricing in a 25 basis point cut, but the chances of this cut increased from 64.0% to 75.4% over the last week (primarily after the PPI print on Friday).

Despite this, Federal Reserve Bank of Chicago President Austan Goolsbee made the following statement on Friday after the release of the PPI regarding the possibility of a March rate cut:

“They (the market) were getting the cart before the horse…What’s going to drive the decisions about rates is going to be the actual data.”

Fed officials have suggested that there will be three rate cuts in 2024 but the market is currently pricing in the possibility of seven rate cuts (see table below).

While these probabilities can and will change, it seems that there is currently a disconnect between what the Fed is suggesting (three rate cuts) and what the market is pricing in (seven rate cuts). I believe the only way you get to seven cuts in 2024 is if “something breaks” or we are knee-deep in a recession.

Or, is that what the market is trying to tell you (i.e., that it believes “something will break” or that we’ll be knee-deep in a recession)? Food for thought.

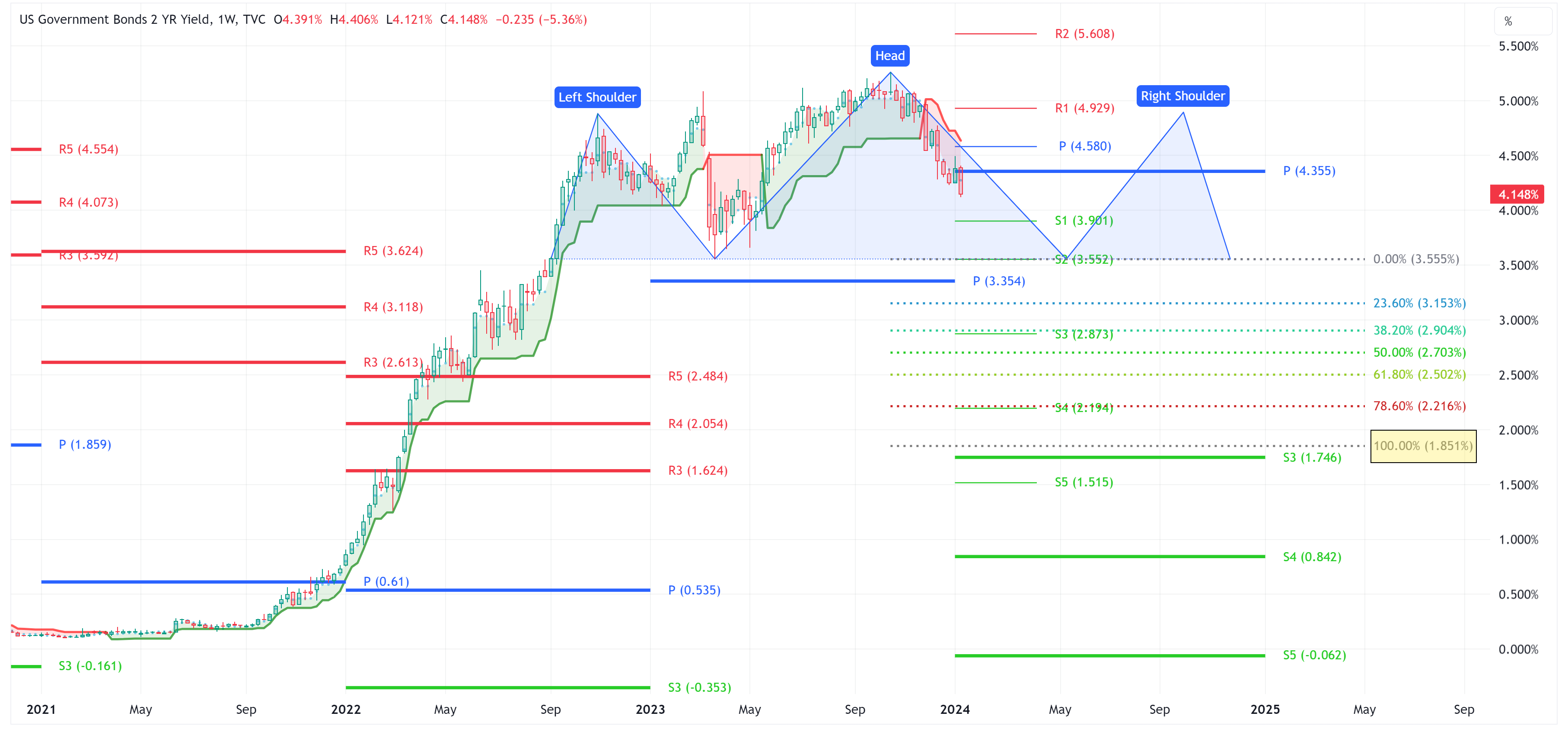

US Treasuries

Let’s look at what US Treasuries are telling us and we’ll use the following charts to directly answer the subscriber’s question I noted at the top.

I’ll start with the US Treasury 2-year and in each of these three charts, I will be looking at weekly data to smooth out some of the noise from the daily price changes.

A couple of quick observations:

The UST 2Yr is currently in a downtrend (i.e., yields are falling) and we can see that not only visually but also as the price is currently below our trailing stop loss.

While it’s still too early to make an official call, we want to watch the chart to see if it develops into a head & shoulders topping pattern. If it does, I am suggesting that the neckline will be ~3.555% and the target will be ~1.851% (yellow highlighted box).

In addition to the trailing stop loss and the head & shoulders pattern, I have placed several horizontal lines on the chart. These horizontal lines are “pivot points”.

Keep reading with a 7-day free trial

Subscribe to Skillman Grove Research to keep reading this post and get 7 days of free access to the full post archives.