What is the Average Investor Allocation to Equities Telling Us?

Spoiler Alert: Subpar "Buy & Hold" Returns and Increased Volatility Over the Next Decade

It is time for the quarterly update of my favorite chart, the “Average Investor Allocation to Equities” chart.

This chart is incredibly important because of the relationship between the average investor allocation to equities and the subsequent 10-year return for the S&P 500.

Very simply, the higher the allocation to equities today, the lower the 10-year return will be for the S&P 500 from that point forward and vice versa.

The blue line in the chart below is the “Average Investor Allocation to Equities” and it maps to the left-hand scale. Where you see the figure 51.7%, this means that on average, 51.7% of the average investor’s portfolio was allocated to equities.

The yellow line in the chart below is the “10-Year Forward Annualized Price Return” for the S&P 500 and it maps to the right-hand scale. Note: the right-hand scale has been inverted for comparison purposes.

You can see visually that these two lines track each other quite well. Further, note the correlation and r-squared statistics in the top left-hand corner of the chart.

Given the tight historical relationship between the two lines, we can create a very simple formula to predict what the 10-year forward annualized returns “should be” for the S&P 500.

The most recent reading for the “Average Investor Allocation to Equities” metric is 44.92%. This suggests that the 10-year forward annualized returns for the S&P 500 should be approximately 0.68%.

While not exactly awe-inspiring, at least it has improved from our most recent high on 12/31/21 when the “Average Investor Allocation to Equities” metric was 51.7% which translated to a 10-year forward annualized return of -3.35%.

Two charts above, you’ll notice that I’ve drawn vertical dashed lines to indicate the cyclical troughs for the “Average Investor Allocation to Equities” metric. Interestingly, the first two periods were very similar in length, 29 years and 27 years, respectively. For the third period, I simply took the average of the first two for illustrative purposes. This would suggest that the trough of the current cycle may not be until ~2037 but only time will tell.

Given where we are in the current cycle, I’m more concerned with how the S&P 500 performed historically from the cycle peak to the cycle trough.

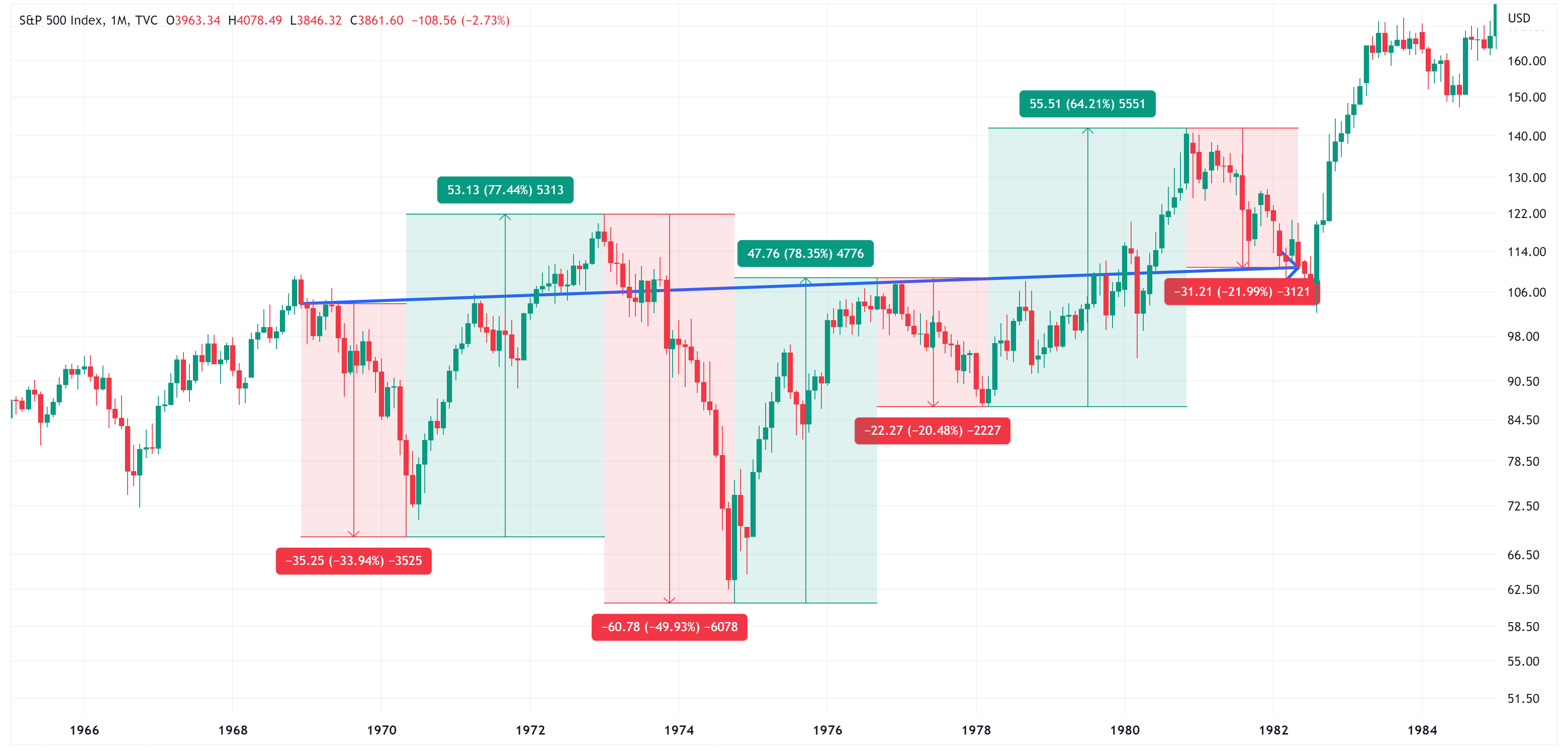

In the first cycle, the “Average Investor Allocation to Equities” peaked at 45.3% on 12/31/68 and bottomed at 21.9% on 06/30/82.

Here is an image of the S&P 500 during that time frame. The blue arrow denotes the period from 12/31/68 to 06/30/82 during which time the S&P 500 had a compounded annual growth rate of 0.40%. Effectively, the S&P 500 moved sideways for 13.5 years yet look at the dramatic swings in returns over that time period.

During the second cycle, the “Average Investor Allocation to Equities” peaked at 51.7% on 03/31/00 and bottomed at 26.6% on 03/31/09.

Here is an image of the S&P 500 during that time frame. The blue arrow denotes the period from 03/31/00 to 03/31/09 during which time the S&P 500 had a compounded annual growth rate of -6.77%. Again, notice the dramatic swings in returns over that time period.

Alternatively, if we zoom out and look at how the S&P 500 performed from the trough of one cycle to the peak of the next cycle (green arrows), we see a completely different story.

From 06/30/82 to 03/31/00, the S&P 500 had a compounded annual growth rate of 15.82%. From 03/31/09 to 12/31/21, the S&P 500 had a compounded annual growth rate of 15.04%.

I noted previously that the projected 10-year annualized return for the S&P 500 from our most recent “Average Investor Allocation to Equities” peak on 12/31/21 is -3.35%. This would equate to a value of ~3,354 for the S&P 500 on 12/31/31. While this is only ~500 points lower than the current value of the S&P 500, it means that the S&P 500 will effectively go nowhere for the next 8 years but will likely be subject to extreme amounts of volatility similar to the previous two examples noted above.

The chart above details four very distinct historical periods. Two were characterized by subpar returns and substantial volatility whereas the other two were characterized by terrific returns. We are now in the fifth distinct period and unfortunately, history would suggest that this period will likely be characterized by subpar returns and substantial volatility.

I believe this translates to an increased need for active management over the next decade. Given the degree to which human emotion has the ability to negatively impact investment decision-making, especially in highly volatile markets, I believe the “winners” over the next decade will be those that deploy some form of systematic quantitative-based portfolio management.

Let me be clear, using a systematic quantitative-based form of portfolio management does not absolve human oversight from the process. Instead, I believe the next decade will usher in the rise of humans working in tandem with Artificial Intelligence (AI) to create more robust forms of portfolio management.

The goal should be to leverage the data-crunching capabilities of AI while at the same time relying on human oversight and investment experience to direct model creation and verify results for real-world applicability.

If done properly, I believe the next decade does not have to result in subpar results for investors and that a systematic quantitative-based approach to portfolio management will likely outperform the traditional “buy & hold” investments.

Until next time…